Credit union Complaints

Credit Unions provide depository and lending services to members of a specific community. The industry experienced growth through the end of 2022 from increased membership and rising interest rates. As macroeconomic conditions improved through 2019, credit unions significantly benefited from increased consumer borrowing as interest rates rose alongside borrowing activity.

However, in 2020, lower demand because of COVID-19 hampered industry activity and growth. Economic uncertainty led consumers to inhibit their spending in 2020, while interest rates declined because the Federal Reserve lowered the Federal Funds Rate to the zero-bound range.

Selected Industry Trends

Factors influencing the Credit Unions industry

Key drivers of the Credit Unions in the US market include Aggregate household debt, House price index, Prime rate, and New car sales.

Financial service products must remain affordable for average Americans, especially those who may be unbanked or underbanked, have invisible credit, or have impaired credit histories. In October, the U.S. Bureau of Labor Statistics' latest Consumer Price Index rose 3.7% during the last year, and the costs for consumer goods such as gas, housing, energy, and other household prices continue to be elevated.

The Federal Reserve continues to maintain a higher federal funds rate, which will likely lead to higher costs of credit cards, mortgages, and vehicle loans. While the unemployment rate currently remains historically low, the personal saving rate dropped to 3.9% in August, down from the pandemic high of 32%.

Ultimately, these costs will be passed on to American consumers. This contradicts the federal administration’s goal of reducing fees for American consumers.

More members are turning to credit unions.

Credit unions are seeing not only an increase in members but also an increase in usage. Members are investing more money with credit unions, and their account balances are rising. We’ll likely see member volume and engagement continue to rise.

Interest rates will continue to rise.

The Federal Reserve is expected to continue raising interest rates in the coming years. Historically, high inflation spreading across the globe requires considerably higher interest rates than the current rate.

In typical situations, people reduce debt when interest rates increase. The current and increasing economic hardships are forcing households to increase their debts despite the higher interest rates increasing volatility.

Industry consolidation

The number of federally insured credit unions declined to 4,645 in the third quarter of 2023 from 4,813 in the third quarter of 2022. In the third quarter of 2023, there were 2,908 federal credit unions and 1,737 federally insured, state-chartered credit unions. The year-over-year decline is consistent with long-running industry consolidation trends.

The number of small companies with few workers

Most credit unions are small companies. According to the National Credit Union Association, nearly three-fourths of all credit unions are considered small, which can be defined as holding less than $100.0 million in assets.

Delinquency rate

The delinquency rate at federally insured credit unions was 72 basis points in the third quarter of 2023, up 19 basis points compared with the third quarter of 2022. The delinquency rate on non-commercial real estate loans was 49 basis points in the third quarter of 2023, 10 basis points higher than in the third quarter of 2022.

The credit card delinquency rate rose to 190 basis points from 130 basis points one year earlier.

The auto loan delinquency rate increased 25 basis points over the year to 78 basis points in the third quarter of 2023. The delinquency rate for commercial loans, excluding unfunded commitments, was 45 basis points in the third quarter of 2023, up three basis points from a year earlier.

Increasing CFPB enforcement

CFPB plans to hire 50% more enforcement attorneys during the next few months. In the CFPB's 2022 financial report, 44% of the Bureau’s workforce was already dedicated to its Supervision, Enforcement & Fair Lending Division.

NCUA

The National Credit Union Administration is the independent federal agency created by the U.S. Congress to regulate, charter, and supervise federal credit unions. The agency’s mission is to provide, through regulation and supervision, a safe and sound credit union system that promotes confidence in the national system of cooperative credit.

It protects credit unions and the consumers who own them through adequate supervision regulation.

- To regulate and generally supervise the credit union sector.

- To contribute to public confidence in credit unions.

- To deter deceptive or fraudulent conduct, practices, and activities.

- To promote high standards of business conduct.

- To protect the rights and interests of consumers/members.

According to NCUA’s 2023 Supervisory Priorities, NCUA continues to review compliance with applicable consumer financial protection laws and regulations for federal credit unions.

In 2022, NCUA examiners requested information about a credit union’s policies and procedures governing overdraft programs to address consumer compliance risk and potential consumer harm from unanticipated overdraft fees. In 2022, the target review activities focused on fair lending (overt indicators discrimination), loan forbearance (mortgages, non-mortgage), Cares Act (consumers reporting protections, Fair Credit Reporting Act)

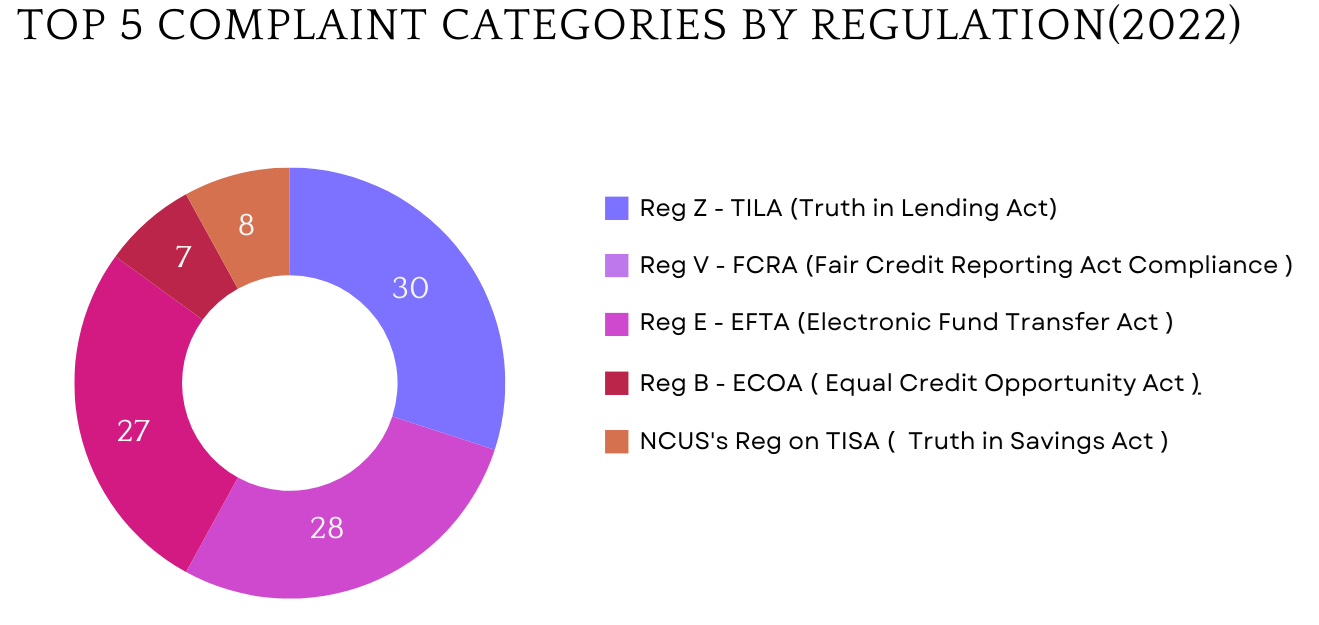

Most cited violations

Complaint trends

Top complaint issues in 2022 and most complained products related to it

CFPB

Community banks and other smaller financial institutions are graduating to the $10 billion-plus asset level in increasing numbers. But $10 billion is also the level at which a depository institution faces supervision and enforcement by the Consumer Financial Protection Bureau (CFPB) for the first time. So, a transitioning institution must meet heightened consumer protection expectations, especially in such areas as conduct risk, fair lending, and its effort to avoid unfair, deceptive, or abusive acts or practices (UDAAPs).

Different consumers require different financial products and services to meet their needs. The CFPB is committed to working with community banks and credit unions to ensure that American families have access to & understand a variety of products, services, and financial relationships, both now and in the future.

The bureau focuses on whether an institution’s policies and practices pose risks to consumers rather than risks to the institution itself. CFPB examiners review policies, programs, and procedures surrounding:

- The nature and structure of products and services;

- The treatment of vulnerable consumers;

- The marketing methods used and

- The level of customer service.

CFPB’s supervision and examination process includes obtaining information about activities, compliance systems, or procedures for certain entities and individuals that offer or provide a consumer financial product or service and their service providers. Examples of monitoring activities include:

Reviewing supervisory and public information about the entity, such as:

- Call report data;

- Complaint data;

- CFPB consumer complaints.

Examiners review the complaint files to identify patterns of issues or significant concerns. Under Violations of Law and Consumer Harm, the CFPB examiner analyzes the following assessment factors:

- The root cause, or causes, of any violations of law identified during the examination;

- The severity of any consumer harm resulting from violations;

- The duration of time over which the violations occurred; and

- The pervasiveness of the violations

Meeting Consumer compliance

Community banks and credit unions are critical in ensuring a fair, transparent, and competitive marketplace for consumer financial products and services.

A credit union’s standards of business conduct, ethical behavior, and its code of market conduct must include preventing mis-selling, tied selling, and misrepresentation of information to members/customers. disclosure of material information, complaints handling, conflicts of interest, and protecting member/customer information. The conduct framework can be summarized with the five principles below.

- Business Practices: Fair treatment to all the members and consumers for the banking products and services. It must be a core component of the governance and corporate culture.

- Fair Treatment and Fair Sales: Treating members and consumers fairly and always demonstrating fair sales practices must be integral to business practices.

- Access to Banking Services: Ensure all credit union members and consumers are granted access to certain fundamental financial services.

- Transparency and Disclosure: Credit unions use plain-language descriptions of products and services to ensure people make informed decisions. Customer support staff must explain this clearly to customers.

- Complaint Handling: Examine all complaints and work to settle them fairly, and track complaints to help ensure practices continue to improve

Credit union compliance teams must plan and enforce internal policies that reflect the regulatory standards delineated by the Consumer Financial Protection Bureau and the National Credit Union Administration.

Compliance failure leads to significant fines of millions of dollars and substantial reputational damage. Bad customer experience and complaints result in customer churn and escalation to the ombudsman like CFPB.

To prevent this, senior Management must:

- Implement the standards of business conduct, ethical behavior, the credit union’s code of market conduct, and related policies, practices, and procedures throughout customer engagement.

- Establish appropriate controls and measures to identify and address potential non-compliance with its standards of business conduct and ethical behavior and the credit union’s code of market conduct.

- Develop a self-assessment program to monitor the credit union’s adherence to its standards and code effectively and a plan to address any areas identified when adherence should be improved.

- Report to the Board regularly on the credit union’s overall adherence to the standards of business conduct and ethical behavior and its code of market conduct